While new business districts lead the way in Mumbai and Delhi-NCR, CBD remains the most attractive in Bangalore

While new business districts lead the way in Mumbai and Delhi-NCR, CBD remains the most attractive in Bangalore

Anuj Puri, Chairman and Country Head at JLL India

While retailers have identified the Office Retail Complex (ORC) format as a good alternative, they are more than ever, willing to look at this format with much more interest in the absence of quality retail space. ORCs offer a higher bang for their buck with comparatively lower rents despite being offered prime ground floor spaces in comparison to premium malls and with weekday footfalls as well as viewership guaranteed to be higher than comparable malls.

With the added benefit of nearby residential nodes, such ORCs at their optimum have the potential to operate as standalone retail malls in respect of the lower floors and generate similar footfalls and business incomes for retailers. This format also offers institutional investors a potentially higher revenue across a diversified tenant base while providing them the key differentiator which may be the ultimate weapon in commercial occupier retention and future rental upside potential. We look at the how this format is shaping up in the tier-I cities.

Mumbai: New Business Districts Drive The Trend

Mumbai is one of the prime tier-I office markets where ORCs are visible across modern office pockets of Bandra-Kurla Complex (BKC), Andheri East, Powai and Navi Mumbai. Hiranandani Powai ORC has the highest rental premium of over 3X, possibly on the back of its added benefit of being an elite neighbourhood residential development.

While the old CBD (Nariman Point) does have a few retail outlets to talk about, it may not feature high on the list of retailers as buildings are of old design and may not offer amenities such as ample parking space, large display area, etc. Also, Mumbai’s CBD area is already proliferated by local F&B outlets and high streets, thereby making the ORC concept somewhat redundant. As a result, retail rents fetch a higher premium over office rents in modern office locations compared to the CBD.

F&B is the most dominant category, as it accounts for 46% of the total retail categories’ presence. Noticeably, this category has adapted to the culture that different ORCs have to offer. For instance, at BKC, expensive fine dining restaurants have made maximum inroads while at Andheri East, most F&B outlets cater to the moderately-priced fine dining categories. Banks (16%) and Electronics-Mobile-Telecom (12%) are the next big categories across Mumbai’s ORCs.

F&B is the most dominant category, as it accounts for 46% of the total retail categories’ presence. Noticeably, this category has adapted to the culture that different ORCs have to offer. For instance, at BKC, expensive fine dining restaurants have made maximum inroads while at Andheri East, most F&B outlets cater to the moderately-priced fine dining categories. Banks (16%) and Electronics-Mobile-Telecom (12%) are the next big categories across Mumbai’s ORCs.

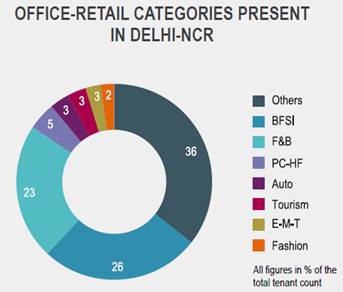

Delhi-NCR: Gurgaon Steals The Show, Followed By Noida & SBD

Delhi-NCR ends up throwing totally different results. While this geography outstrips all others in terms of size of the ORC retail format, the tenant mix is also quite at variance. The dominant category here comprises of Others, which is a heterogeneous mix of groceries, medical stores, property brokers, laundry, courier services, jewellery stores, printing services and stationary outlets.

BFSI makes up for the next highest tenant presence, closely followed by F&B. The remaining categories remain peripheral players who take up space based on the potential value they can derive from their store locations. It is interesting to note that most of such formats and consequently stores are located in destinations which are well-established office corridors.

Even in Gurgaon, the NH-8 and MG Road office corridors are significant contributors, while in the SBD, office corridors such as Jasola, Nehru Place and Saket are the major contributors.

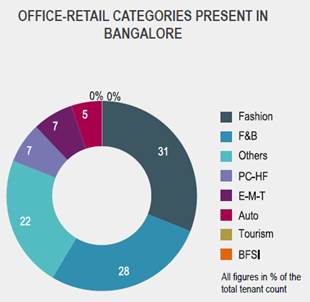

Bangalore: The Only City Where ORCs Thrive In The CBD

The Bangalore office market is predominantly driven by IT/ ITeS occupiers largely confined to huge campus developments. These IT developments only offer the opportunity for a captive audience for retailers, though such numbers may also be quite high as IT firms in Bangalore typically occupy entire towers/ wings of larger office developments.

The commercial developments in Bangalore are largely in the city centre and surrounding areas. The city centre is itself a prominent retail hub and in such a scenario taking-up space in commercial office buildings in the vicinity makes perfect business sense for retailers as they not only cater to the shoppers but also make huge rental savings by opting for ORC formats over the high streets.

The proximity to the city centre is reflective in the tenant mix of ORCs in Bangalore. While generally, Fashion does not figure prominently in the retailers who occupy such formats, in Bangalore, it is visible in the Fashion category dominating. ORCs in Bangalore are a part of the shopping centre of the city than creating a standalone office district. F&B follows a close second as this category has maximum traction with shoppers and office goers alike.

Given the lack of quality retail space across the top-3 Indian cities, ORCs would definitely see good traction at a time when many domestic and international retailers have made plans for expansion. Each ORCs have their unique characteristics making them discerning amongst select categories of retailers. It is only a matter of time before we witness a wide range of retailers expressing their intention to have their presence felt in ORCs. Increased demand and rising premiums could potentially attract a lot more office developers to offer mixed-use developments in the future.

Given the lack of quality retail space across the top-3 Indian cities, ORCs would definitely see good traction at a time when many domestic and international retailers have made plans for expansion. Each ORCs have their unique characteristics making them discerning amongst select categories of retailers. It is only a matter of time before we witness a wide range of retailers expressing their intention to have their presence felt in ORCs. Increased demand and rising premiums could potentially attract a lot more office developers to offer mixed-use developments in the future.