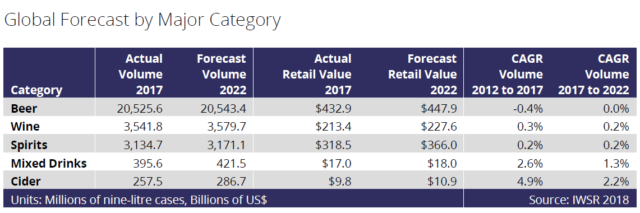

Global value growth is forecast for all major categories over the next five years

Global alcohol consumption is forecast to grow by 147.1m nine-litre cases by 2022 to reach 28bn cases, and grow $78.7bn in value, according to the recently released IWSR 2018-2022 Forecast: Volume and Value Data. Total wine will see the largest growth (+37.8m cases), followed by spirits (+36.5m cases).

Most notably, the global beer market is expected to return to growth in 2018 following a poor 2017 in many markets, but then lose volumes year on year to 2022. Despite declining beer volumes, global beer market value is expected to grow year on year. China, US and Russia, where domestic beers are all in decline, are the main contributors to the drop in beer volumes.

Within the wine category, still and sparkling wine are leading the growth, while fortified, light aperitifs and other wines are all expected to decline. The US, Russia and Brazil are predicted to be the largest-growing markets for still and sparkling wine between 2017 and 2022.

Spirits will see mixed fortune with strongest global growth predicted for whisky, followed by gin and genever, and agave-based spirits. Vodka is forecast to see the largest drop mainly due to continuing declines in Russia. Rum and brandy are also forecast to decline due to drops in low-priced brandy and value rum. However, when looking at the premium-and-above segment, all spirits categories are expected to grow. The IWSR’s forecasts have taken into account tariffs which have been placed on US whiskey in some markets.

The US will continue to be a key market with top growth for wine and spirits, including US whiskey, Irish whiskey, Canadian whisky, tequila, mezcal, Cognac/Armagnac and vodka. The leading growth market for gin will still be the UK, and France is expected to be the lead growth market for rum.

Vietnam, Mexico and Brazil are forecast to increase the most for beer, while Germany will lead growth for low-alcohol beer. Romania is poised to show top growth for cider, while Japan continues to lead mixed drinks growth.

The IWSR is widely seen as the most authoritative data source on the beverage alcohol market. The IWSR’s unique approach to forecasting has proven to be reliable. Comparing last year’s forecast for 2017 with actual 2017 data, the IWSR’s forecast at a global level differed by just -0.4%.

About the IWSR

![]()

The IWSR is the leading source of data and analysis on the alcoholic beverage market. The IWSR’s database, essential to the industry, quantifies the global market of wine, spirits, beer, cider and mixed drinks by volume and value in 157 countries, and provides insight into short- and long-term trends, including five-year volume and value forecasts.

The IWSR tracks overall consumption and trends at brand, price segment and category level. Our data is used by the major multinational wine, spirits and beer companies, as well as financial and alcoholic beverage market suppliers. The IWSR’s unique methodology allows us to get closer to what is actually consumed and better understand how markets work. Our analysts travel the world in order to meet over 1,600 local professionals to capture market trends and the ‘why’ behind the numbers.

About the IWSR 2018-2022 Forecast: Volume and Value Data

The IWSR 2018-2022 Forecasts covers 157 countries from 2018 to 2022. Forecasts are split by category, price band and country. The IWSR 2018-2022 Forecasts comprise an online database, a global summary with regional and category overviews, and 65 individual country forecast reports. Volume and value forecast data is accessible via the IWSR Global Database.